Not unless you’re a business paying for a health plan for your employees. For individuals, the Canada Revenue Agency (CRA) has a has a whole list of health care expenses that are eligible for the Medical Expenses Tax Credit. This tax credit is non-refundable meaning it won’t be paid out if you already don’t pay taxes but can lower your health-related spending by up to 20%.

Common health expenses you can claim include dental visits, laser eye surgery, diapers, hearing aid, and even medical cannabis. It’s important to get to know this list so you can account for all your health spending and claim it. The list is quite large.

Are Health Benefit Plan Premiums Eligible for the Tax

Credit?

Yes. Health benefit plan premiums that you pay to private

health insurance companies are eligible for the Medical Expenses Tax Credit

which is interesting because it allows for you to access this tax credit even

if you’re healthy.

When you’re most healthy is the best time to institute a private health benefits plan because insurance companies exclude pre-existing health conditions and their associated treatments (including prescription drugs) on all their best plans. You can get unlimited prescription coverage on conditions that you don’t already have but you would be limited to $2,700 prescription drug coverage limits on anything pre-existing. Health benefit plans become far less attractive when you need to cover pre-existing health conditions because the insurance providers price in the assumption that entire limits will be used.

Plans are available for those who need to cover pre-existing

conditions, but benefits limits are significantly lower, and prices are

exceedingly higher.

This tax credit is only another incentive for you to plan for what is inevitable. Life is finite and the government wants your money. The best way to deal with these inevitabilities is through planning.

How Does the Medical Expense Tax Credit Work?

Add up all your eligible health expenses for the year then

deduct it by the lower of either 3% of your net income or $2,352 (2019),

then multiply the sum by 15% plus your lowest provincial marginal tax rate.

This is how it’s calculated in the background but all you would have to provide

is the sum total of your annual eligible health expenses. This would be claimed

on lines 330 or 331 of your annual personal income tax return. Sounds

complicated? Here is a calculator to add up how much this credit would represent

for you.

Even if you haven’t started planning and you’re don’t currently have a spotless bill of health, it’s not too late. Often it will still make sense to purchase a medical plan knowing they will exclude coverage on a prescription you take because prescription drug costs vary widely. Standard blood pressure pills often cost under $20 every 3 months while some Cancer drugs cost over $4,000 per month and aren’t covered by provincial health insurance plans in any way. There’s still a wide gap of coverage by provincial health plans for those with diabetes and that condition can be debilitating financially.

Read more

Traveling can produce some of the most enlightening experiences. Seeing how other people around the world carry on their day to day life humbles the mind while exotic locations calm the soul. We live busy lives and it’s cold in winter.

Plus, there’s a lot to see out there

We’re fortunate as Canadians in that we have the means not only to travel but to travel safely. Those of us who do travel should travel safely. We’re used to having at least basic public healthcare as a right here in Ontario but it’s not like that everywhere. While abroad, it’s important you understand how to deal with medical emergencies and healthcare. Have the means.

If you have valid Ontario Health Insurance Plan (OHIP) coverage and you leave the country, you have some coverage but it limited. They will reimburse $50 per day for outpatient healthcare billing (the doctor) and a maximum of $400 per day of inpatient care (hospitalization), regardless of the severity of the situation and only for a limited period of time. It certainly would not have the authority of either private health insurance or a wad of cash in a foreign hospital. Some places are generous, others aren’t.

It’s not advisable to rely on OHIP while abroad

If you have valid OHIP, travel health insurance is generally less expensive because you can always be taken back home for care. It’s also easier to get pre-existing medical conditions covered. If you don’t have valid OHIP and are staying abroad, you would need expatriate health insurance. If you’re emigrating then you would also have public and private health insurance options in your country of immigration.

It’s advisable to try to keep your OHIP coverage if you’re not emigrating and if you can. Pre-existing health conditions are more easily covered and prices are generally lower with traditional travel health insurance.

Get a Travel Insurance Quotes

In order to maintain your OHIP coverage, you can’t leave the province for more than 212 days in any 365 day period unless you have lived in the province for at least 153 days the two years prior. In the event that you have, OHIP validity will maintain for two years. You should start looking at expat health insurance only when you are in your second year abroad.

Get Expat Health Insurance Quotes

If your returning to your home province from expatriation to make Ontario your residence again, and you have lost your OHIP coverage, you will be required to wait 3 months to regain coverage. The same applies if you are immigrating to Ontario. You can get private health insurance to bridge that 3 months. Private health insurance will cover you for emergency care, hospitalization, paramedical coverage, prescription care and some dental treatment. It’s typically referred to as visitors to Canada health insurance but it’s not just for visitors.

Get Visitors to Canada Health Insurance Quotes

It’s important that when looking at private health insurance that do business with a provincially licensed broker. You should also look at plans from many different companies. A good broker will typically be able to send you price quotes from many different insurance companies all at once at no extra charge. Ask about exclusion clauses in the policy to consider how they may apply to you. If concerned, examine policy wording as again, a good broker should be able to provide.

In order for traveling to be a positive experience, it’s wise to cover the important bases prior to leaving. No traveler wants to deal with anything as serious as finances in a health emergency. Take care of yourself.

Read more

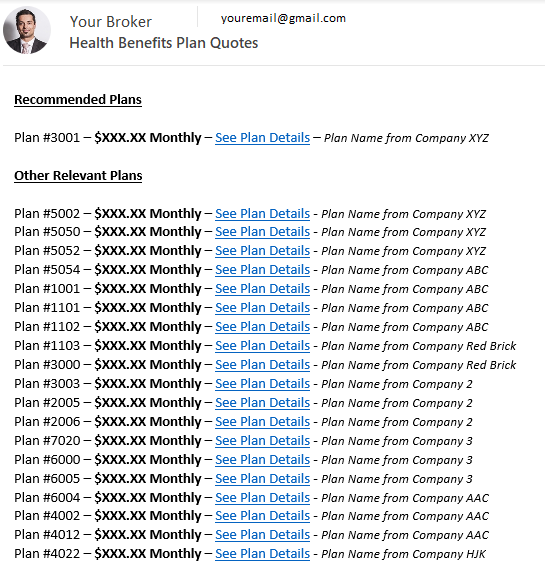

Skip calling all the insurance companies for rates and plan summaries. We’ll send you a menu of all the health benefit plans from all the providers with price quotes tailored to you and your family. We’re skipping all the baloney.

Get your Tailored Health Benefits Plan Menu

What happens next?

After requesting price listings, you’ll get an email within 30 minutes providing your broker’s name and contact information. There will be a disclosure in the email for the purpose of transparency, a link to their provincial license as well as their social media. You can get to know your broker as much or as little as you want.

If you request your quote during business hours, you’ll get a

menu of options from your broker within 2 hours. If your request is after

business hours, you can expect it the early the next business day. You will get

a phone call from your broker introducing themselves. If you prefer to only

communicate electronically, that’s okay, let your broker know.

Your broker will further simplify things for you by making a recommendation, but we don’t care which provider you use. We just want your business and to keep it. Let us know how we can do that.

All the plans are numbered, and the summaries are presented in a standardized way which really helps in comparing what the plans cover. If you’re looking for good massage therapy coverage, then plan #1102 can be a good option. If you need affordable major dental coverage that starts quick, plan #6005 is a good one. It can often save you money on the dental alone. To add, our service doesn’t cost you anything extra. You could go to all the insurance companies directly and it would cost you the same amount.

If you want coverage on existing medical conditions or prescription, that’s fine. We’ll send all the plans that available that don’t require a medical questionnaire. If you recently left a group benefits plan, you can get decent prescription coverage that covers existing medication. Plan #2024 is no doubt a high-end plan, but it can cover $200 a month of existing prescription expenses.

End of story.

Read more

As Canadians, we’re fortunate to have access to a public healthcare system. We hear these horror stories of people getting 4, 5 and even 6 figure medical bills in the US, dismissing that poor health can cost us our livelihood, even here in Ontario. We have good critical care but chronic illness is treated as an afterthought. Unless your condition is acute, degenerative or deadly, you have to push for public resources to engage healing. You need a referral for diagnostic tests or specialists and waiting in queues can be long.

Having a proper health benefits plan is a game changer in managing your health because it removes the main reason to delay treatment. It’s expensive to pay for medical specialists and diagnostics out of pocket. They’re not a fun expense either. I call it defensive spending because it’s to maintain your quality of life rather than improving it. If it’s the other way around then you’re likely waiting too long to deal with health issues. Kind of like a gym pass, the psychological effect of paying for preventative health services in a health plan will push you to use them which inevitably makes you healthier. People with health benefits are healthier.

Get a Health Benefits Plan Quote

In looking at health benefit plans; you want to get as much as you can for the money. To do that, you should get a plan before you need it. Health plans are way more accessible when you don’t have existing health conditions and medications that need to be covered. If you already have an issue to deal with you can still save money with a health plan but you have to choose the right one. Blue Cross health benefit plans come with a discount program called the Blue Advantage. Using a discount program is the easiest way to reduce your health spending if you’re already dealing with health issues. Blue Cross is the only insurance company offering an extensive discount program with their health benefit plans making them an ideal option.

With Blue Cross, Blue Advantage offers discounts up to 60% on lenses and frames for vision care related spending. If you choose one of their dental hygenist partners, you can access a 20% discount which can be used on top of the dental benefit you have purchased on your Blue Cross plan. Because all discounts can be used on top of existing benefits that the plan provides, the depth of savings is higher than any other plan. You just have to be flexible. There are also discounts at gyms, for physiotherapy, acupuncture, chiropractic care, spinal decompression, nutritional counseling, smoking cessation programs, senior services and a multitude of medical devices. There are more discounts than I can reasonably list.

If you already have a health issue, the Express Plan by Blue Cross will offer you a higher level of coverage for the cost than counterparts because of the Blue Advantage discount program that comes as part of the plan. Not only can the discounts be used for existing medical issues but the coverage can too (with minor exceptions). By stacking Bluecross Express Plan coverage and BlueAdvantage discounts, you can save money on health expenses over the short and long term.

Being proactive in the process of healing is the key to good health. You need to understand your ailments and have the resources to harmonize your health before issues turn into real problems. While awaiting the next OHIP covered step in your healing plan, you should educate yourself by meeting with alternative specialists. See a naturopath, speak with an osteopath, try acupuncture, speak with a psychologist, see a dietician, dive into meditation, try massage therapy, aromatherapy or lose yourself in the jungle. It’s surprising what stress can do and one person won’t have all the answers.

Remove the biggest barrier (which is money) today by getting a quote for a health benefits plan.

Read more

You may have heard of Critical Illness (CI) Insurance through your Insurance Advisor or at the bank when applying for mortgage insurance. A relative newcomer to the insurance industry, CI insurance originated in South Africa when a heart surgeon by the name of Dr. Barnard found that, although he was able to help his heart attack patients live longer, their finances were suffering due to the debilitating cost of the medical treatment and post surgery care. He developed an insurance concept in response to this need that would provide financial assistance to the patient allowing him/her to recover without having to worry about the cost of care or how they were going to meet their everyday financial obligations while they were off work.

CI insurance first came to Canada in 1995 and is only starting to become known thanks to the advisor and banking networks. There are essentially two ways one can purchase CI. The first is as a personally owned policy through the advisor network. In this case, the client has full control of how the proceeds are used since these policies pay out a lump sum in the form of a cheque upon diagnosis of a critical illness as long as the patient survives a period of 30 days. The funds can be used to pay for medical care not covered by OHIP such as experimental drugs or for care sought outside of Canada. Other possible expenses that could be covered include mortgage payments and other monthly obligations that may otherwise fall behind if the patient is unable to return to work right away.

The second method of purchasing CI insurance is through your mortgage provider when you renew or apply for a new mortgage. The policy is tied to the mortgage and any proceeds are used strictly for paying off the mortgage or continuing your mortgage payments for a set amount of time, usually up to one year. As you can see, there is less flexibility as you do not control how the proceeds are allocated. For this reason, it is well worth the time and effort to apply for personally owned coverage through an Advisor.

The three top illnesses covered by CI are Heart Attack, Stroke and Cancer. These three illnesses alone represent over 85% of the claims for CI insurance. Most companies start with these three in their base policy, adding over 21 additional illnesses to their more comprehensive plans. There are also several options that can be added to enhance protection. One option that is worth mentioning is the return of premium rider. With this rider, the insurance company guarantees they will refund all your premiums paid to a specific date as long as no claims were made. The contract is surrendered at the time you decide to exercise this option and it is available as early as 10 years into the contract. The return of premium feature makes it easier to purchase CI coverage knowing that if you do not become ill, you will get all your money back.

Unfortunately, not everyone is a good candidate for CI insurance. For instance, individuals who have a family history of critical illness will have a harder time obtaining coverage, particularly if two or more direct family members have suffered from a critical illness in the past. However, in general, if you are in your 30’s or 40’s, have a family that is dependent on you, or you are single and would not have the resources to care for yourself and meet your ongoing obligations if you were to become critically ill, then it is highly recommended that you consider a personally owned CI insurance policy. My advice is to discuss CI insurance with your Advisor so that he/she can determine whether you qualify for this important coverage.

Read more

Unlike home or car insurance, Disability and Critical Illness insurance are not compulsory and many people hesitate to purchase these important policies due to the cost and the possibility that they may not even end up using the coverage at all. The insurance industry is aware of this fact and has come up with a solution called a return of premium option that makes buying these policies easier both psychologically and financially.

The better quality Disability policies generally provide a return of premium option in one of two forms. The first option involves the return of 50% of your premiums on surrender of the contract as long as the contract was in force for a minimum number of years, usually 10. The calculation of the return of premium is based on just about all the premiums paid into the policy including the policy fee and the amount paid for all riders including the return of premium rider itself. Any claims made during the life of the policy are deducted prior to calculating the amount owing. If claims exceed a certain percentage, the return of premium will not be available. In this case, the client will have paid an extra premium for the chance that he may not have claimed. This can be viewed as insurance on insurance. The real benefit is realized when the client makes very few or no claims during the life of the policy. In this case, the return of premium rider is a good investment.

The second type of return of premium is fairly new in the industry and involves a return of half of the premiums paid after periods of either 7 or 8 years throughout the life of the contract. If a return of premium option is exercised, the policy continues in force as long as the client continues to pay the monthly premiums. You can either withdraw the funds in cash or you may opt to leave the funds on deposit with the insurance company who then draws from those funds to pay future premiums for the next 7 or 8 years.

Generally, the cost to add the return of premium option on a Disability policy ranges from 25-50% of the cost of the rest of the premium with the return of premium on surrender being at the lower end of the scale and the return of premium after 7/8 years being the most costly.

Critical Illness policies also offer a return of premium option in two forms. The first is a return of premium at death should the cause of death be other than a Critical Illness. The additional premium for this option is minimal, costing about half a percent of the total premium. In addition to this, you can also choose the return of premium on surrender of the contract with the stipulation that the contract must be in force for a minimum number of years, usually 10. You must specify at the time of application which return of premium option you want, and the earlier the option date, the more expensive it will be. For instance, a return of premium option that can be exercised as early as year 10 will run you about 70% of the base premium, whereas choosing the option at the expiry of the contract will cost about 45% of the base premium, depending on your age at the time of application. Although Critical Illness return of premium is quite costly, it is, in fact, a win-win situation. If in the unfortunate event you become critically ill, you will receive the full benefit, but if you don’t end up claiming on the policy, you will receive all of your premiums back. You want to make sure, however, that if you choose the return of premium option, that you fully intend to keep the contract in force until at least the first option date, otherwise, all those extra premiums will have been paid for nothing. One other thing to note is that many companies are now offering the return of premium on a scaled basis. What this means is that if you choose a return of premium option after 10 years, you will receive 50% of your premiums back in year 10, 60% in year 11, 70% in year 12 etc until the full 100% becomes available in year 15.

Although adding a return of premium option on your Disability and Critical Illness contracts can add significantly to the cost, it does provide for peace of mind that at least you will receive part or all of your money back in the event that you do not end up claiming on your policy. This cannot be said for auto or home insurance, yet, we as consumers have become accustomed to paying these premiums. So it follows that if you insure your house and your car, why would you not insure your health and future income earning potential when the out of pocket cost is 0%-50% of the actual premiums?

Read more